The Next Phase of the Collapse of 2021

How to Protect Your Finances and Build Wealth Swiftly

Click here to download your free endangered lists and special reports now. Or read on for the full transcript …

- Find true financial safety in a very unsafe world

- Build a protective firewall around your stock and bond portfolio

- Safeguard your retirement

- Avoid losses in your real estate and business

- Go for some of the largest crisis profit opportunities we’ve ever seen

Dear Friend,

This is a very solemn moment in history, a time for prayer, but also a time for action.

The coronavirus pandemic is creating a financial nightmare in America.

It's unleashing a chain of devastating economic events that will change almost everything in your life.

And if you think what has happened so far is shocking, brace yourself for what's coming next.

My name is Martin Weiss, and I'm the founder of Weiss Ratings, a company I began a half-century ago to help Americans of all walks of life keep their money safe in good times and in bad times like these.

I'm not here to frighten you. God knows there's more than enough fear in America today.

Rather, I'm here to give you the facts about how this crisis will impact your money and how you can find safety in an unsafe world. Because our financial world today is not safe, and this isn't the first time I've said so.

For many months, we have published lists. I call them "endangered lists," naming thousands of stocks, ETFs and mutual funds that are vulnerable to a crash, plus thousands of banks that are vulnerable to a financial crisis just like this one.

Then, in December of 2019, I warned of a severe recession and debt crisis in 2020.

And as the stock market reached a peak, we gave the signal to sell.

As a result, we not only helped investors avoid the stock market crash of 2020, we also helped them make money in the decline. Today, in this time we have together, I will tell you how you can do that, too.

I will give you a clear roadmap about what’s likely to happen now and over the next few months.

When the stock market was peaking, we issued a landmark trade alert, telling our subscribers to sell all their long ETF positions, including SPY (which tracks the S&P 500) and QQQ (which tracks the Nasdaq 100).

I will give you immediate free access to our lists of companies and investments that are in gravest danger … and to our lists that will guide you to those that are the safest.

Plus, I will walk you through seven steps you can take right now. With these simple steps, you can protect everything you have: Your stocks and mutual funds, your 401 and IRA, your real estate, and your savings.

With these steps, you can also turn this crisis into an opportunity to swiftly build your wealth.

This is urgent, because this is no ordinary financial crisis.

It's far bigger than anything we've ever experienced in our lifetime, and it's striking with far greater speed. Almost everything you own is in jeopardy, even things that you thought would be safe.

Not just money you have in stocks, but also money you have in bonds and even banks.

Not just right now, but for many months to come.

All of those assets are tied to the fate of the economy.

Even if this crisis does not turn out to be as bad as we fear, you could still lose half of your money, and in many situations, you could even lose all your money. I'll explain why in a moment.

But before we go there, I want to be perfectly clear about one thing: This will not be the end of America: Our country's forefathers — and our own ancestors — were able to overcome threats that were even worse. We will ultimately overcome this threat too.

Trouble is, it will take quite a few years to get there.

I don't want you to suffer through quite a few years, not even one year or one month.

In fact …

If you take the few simple steps I will outline today, not only can you survive this crisis with your money intact, you can actually come out ahead of the game.

When you do that, you won't be the only one who benefits. Everyone in your family will be better off, too.

And when the economy is finally ready to recover, the country will need savers and investors like you — people who keep their money safe now, who wait for the right time, and who reinvest in America to help bring about a true, lasting recovery.

Today, though, it's far too soon to talk about the recovery.

The crisis is just starting. Thousands of companies, big and small, will go bankrupt. Millions of people will be thrown out of work. Even the rich will take a big hit, and they have the most money to lose.

Surely, the government can bail out some companies and some states some of the time.

But can the government bail out everyone all the time? Can the government stop the stock market from falling? And here's the big question: If the U.S. government spends too much money to bail out everyone else, who will bail out the U.S. government itself?

For now, what I can say for sure is this: No matter what the government does, this crisis will make the last crisis, the Debt Crisis of 2008, pale by comparison.

When the dust settles, the collapse of 2020 will destroy the American dream for millions. And for most American families, nothing will ever be the same again.

I don't want that for you.

Now, maybe you're thinking that, “once the pandemic crisis ends, then the financial crisis will end, too.”

If I were you, I would not bet on that either.

You see, long before the coronavirus appeared, we already had all the ingredients of a serious financial crisis here in America.

This crisis began a long time ago with years of government manipulations; years of bad advice, dishonest ratings, and lies that lured millions of homeowners into debt; that spurred millions of investors to throw caution to the wind; that drove nearly everyone to take unprecedented risks with their hard-earned money.

If you find that hard to believe, I'll give you all the facts here in a moment. I'll show you how most people, most companies, even most banks in America are not prepared for this crisis.

I'll tell you exactly how many of them were already in deep trouble before the crisis began.

Fortunately, a small minority of investors will escape the dangers and even use this crisis to build substantial wealth. If you act promptly on the simple recommendations I'm about to give you, you could be one of them.

You see, almost 50 years ago, I started my own rating and research company, the successor of my father's company, which he started decades before that.

Since then, we've built a massive database of 57,000 companies and investments: stocks, ETFs, mutual funds and financial institutions.

Today, that entire database has been modernized by a team of analysts, mathematicians and data scientists, using advanced computer models.

That's how we warned in advance about the bank failures of the 1980s.

That's how we warned in advance about the Dot-Com bust of the early 2000s and the great Debt Crisis of 2008.

But we don't just issue warnings, we also issue ratings, the Weiss Ratings. We provide a letter grade from A to E on nearly every stock, every ETF, every mutual fund, and every financial institution in America.

With those ratings we name the stocks that are likely to fall the most; we name the banks that are most likely to go bankrupt.

In the last debt crisis, for example, we warned about nearly every major institution that failed and we did so months in advance.

- We named Lehman Brothers as a candidate for failure 182 days before it went bankrupt.

- We named Fannie Mae over one year in advance …

- Citibank, Wachovia Bank, and Washington Mutual Bank, 51 days in advance …

- General Motors five months in advance, and many more.

Among the 465 banks that failed during and after the debt crisis, we warned consumers about 464 banks.

(We missed one, but that was only because the bank had committed fraud, which they kept hidden from everyone.)

These kinds of on-target warnings prompted Worth magazine to say “Weiss’s record is so good compared to that of its competitors, consumers need look no further” and …

The New York Times to say “Weiss was the first to see the dangers and say so unambiguously.”

Barron’s wrote, “Weiss is the leader in identifying vulnerable companies.”

Louis Rukeyser of Wall Street Week wrote that “Weiss provides a tougher service.”

Chris Ruddy, founder of Newsmax and a close friend of President Trump, said, “Weiss’s prediction of the current economic crisis is uncanny.”

You see, our roadmap for surviving and thriving through a crisis wasn’t thrown together after the crash hit. It’s built on a foundation of crisis investing that goes back nearly a century, to the Crash of 1929 and the Great Depression of the 1930s.

Martin Weiss’s father, Irving Weiss, borrowed $500 from his mother and turned it into about $100,000 in the great bear market of the early 1930s. You could do something similar today with much less risk.

That’s when my father and mentor, Irving Weiss, discovered the foundational secrets behind our business today, and that’s what led him to make a final prediction before he passed away.

That prediction is literally coming true right now in real time. So let me roll back the clock to show you how he knew …

Irving Weiss first went to work on Wall Street in the late 1920s as a customer's man, which nowadays they'd call a “stockbroker.”

The stock market of the 1920s would be eerily familiar to anyone living through the crisis of 2020: It was enjoying a roaring bull market that was unusually long, just like it had been doing in recent years.

And the market was unusually out of sync with the tough times that most working American families were experiencing, also much like it was in recent years.

So when the Dow Jones Industrials kept going up in the first 10 months of 1929, my father didn't trust it.

He didn't trust the disconnect between the “great times” on Wall Street and the tough times in the neighborhood where he lived.

He didn't have many clients yet, just friends and family. But he told them to get the heck out of the market.

In 1929, Wall Street veterans laughed at Weiss’s warnings of a crash. “He’s just a kid,” they said. “What does he know?” As it turned out, he not only knew to get his clients out of the market before the crash, he also learned to turn the decline into an opportunity to build substantial wealth.

In his office down on Wall Street, the veteran stockbrokers laughed at him. “Weiss is just a kid,” they said. “What does he know?”

But then came Black Monday, October 28th 1929. The market plunged the equivalent of about 2,500 points in the Dow Jones of today. Then, on the next day, on the Tuesday, it plunged the equivalent of another 2,500 points.

It was like a 5,000-point crash in just 48 hours.

Suddenly, Irving Weiss was a hero, and suddenly the word got around that he was the only one who saw it coming.

That’s when he decided to do more, much more. He decided to actually make money from the crash.

He had learned accounting in school. So he knew the numbers really well. He collected data on as many companies as he could. He put the numbers down on large, green sheets that bookkeepers used — spreadsheets, actually.

And he created a series of formulas that would later become the foundation of our computer models.

Using his formulas, he identified the companies that he thought were the riskiest. He called them “Dogs of the Dow.”

And then, in April of 1930, after a big stock market rally, Irving borrowed $500 from his mother, and he started selling short the stock market Dogs.

When the market plunged, he took profits. Whenever it rallied, he shorted again.

And by the time the Dow hit rock bottom in 1932, he had over $100,000, or nearly $2 million in today's money.

That was about 200 times his money.

Not bad for a young man who was just a rookie on Wall Street, right?

So you’re probably wondering: If stocks fall further in this crisis, could you do something similar — both to protect your wealth from the downside and to build your wealth swiftly as this crisis unfolds?

The answer is yes.

And it all comes back to …

One of the last predictions my father

made before he passed away …

He warned that someday the stock market will crash again, and someday America will suffer a second Great Depression. He didn’t say exactly when it might happen, but he did tell me how it would happen.

“The first big crisis,” he said, “will hit the mortgage market. People will default on their mortgages. Home prices will collapse. Big banks will fail. But the government will come to the rescue by printing and spending trillions of dollars. And within a few of years, they will manage to turn things around.”

He was right. That’s very close to what actually happened in the Debt Crisis of 2008.

“But the second time it happens,” he predicted, “the crisis will be so severe, all the government’s money printing and all the government’s spending will still not be enough to put things back together again. Eventually, the country will recover, but it’ll take years, many years for that to happen.”

Well, now, that second crisis is upon us, and it’s so new, it’s so different it still has no name.

Some people call it “the Coronavirus Crisis.” I call it “the Financial Pandemic.”

But whatever name you give it, the dire reality is staring us in the face …

According to the U.S. Labor Department itself, more people have been thrown out of work more quickly than during the Great Recession of 2008-2009 and even during the Great Depression of the 1930s.

And according to a Bloomberg report, more businesses are expected to fail than at any time in history.

But if you think that’s bad, consider this,

Jerome Powell, Chairman of the Federal Reserve, says we’re going to see economic data that’s “worse than any data we’ve ever seen.”

The U.S. Congressional Budget Office predicts that a deep recession will continue for at least two years.

And JP Morgan Chase says it will take at least 10 years for the economy to recover.

Every aspect of this crisis is already more severe than it was the last time, in the Housing Bust, Debt Crisis, Great Recession.

And this is just the beginning.

So, before you and I part today, I will give you access to my family's and my company's most precious crisis-investing guidance. That includes our current endangered stock lists and our lists of the strongest companies, too.

But I must warn you …

Our endangered lists are very long, and that’s the best evidence I can give you to prove that this is not just a pandemic crisis.

It is also a financial crisis that has been building up for years. Even before this crisis began, our endangered lists included more than

- 5,000 common stocks …

- 6,000 ETFs and mutual funds …

- 1,000 banks and credit union with insufficient capital to withstand an ordinary recession, plus …

- Another 3,000 banks unprepared for a depression.

And now, I’m sad to say, as this crisis unfolds, our endangered lists are getting even longer.

So the probability is high — and getting higher — that most of your stocks and mutual funds and even your bank is on one of the endangered lists.

Now, not all companies are in bad financial shape, mind you. There are still strong ones, and I’ll give you those lists, too.

But whether good or bad, you just need to know. And you need to know now, before this financial pandemic gets worse.

Plus, there’s one more thing I want you to know: Until now, we charged a small fee for folks to access our ratings.

You see, we’re not like Standard & Poor’s, Moody’s, and Fitch, because when they issue a rating on a company, they get paid by that same company for the rating.

Their ratings are effectively bought and paid for by the rated companies.

Many smart people think that’s a serious conflict of interest, and I agree. Plus, it’s also one of the reasons why millions of people who followed their ratings lost so much money in the last debt crisis.

We never do business that way. We have never taken — and never will take — a dime from the companies we rate.

Our only source of revenues has been the end user of our information, average people who want to get safe and make some money, too. But because of this crisis, I don’t want any barriers between our ratings and your safety.

So starting today, I’ve opened up access to all of our ratings lists for free. And I’ll show you how to get them before we’re done here today.

First though, I want to answer that big question I raised earlier and that’s probably on your mind right now too:

Will the government be able to print and spend enough money to make a lasting difference for you and your family?

Sure, the government can bail out a select group of companies that qualify for special loans.

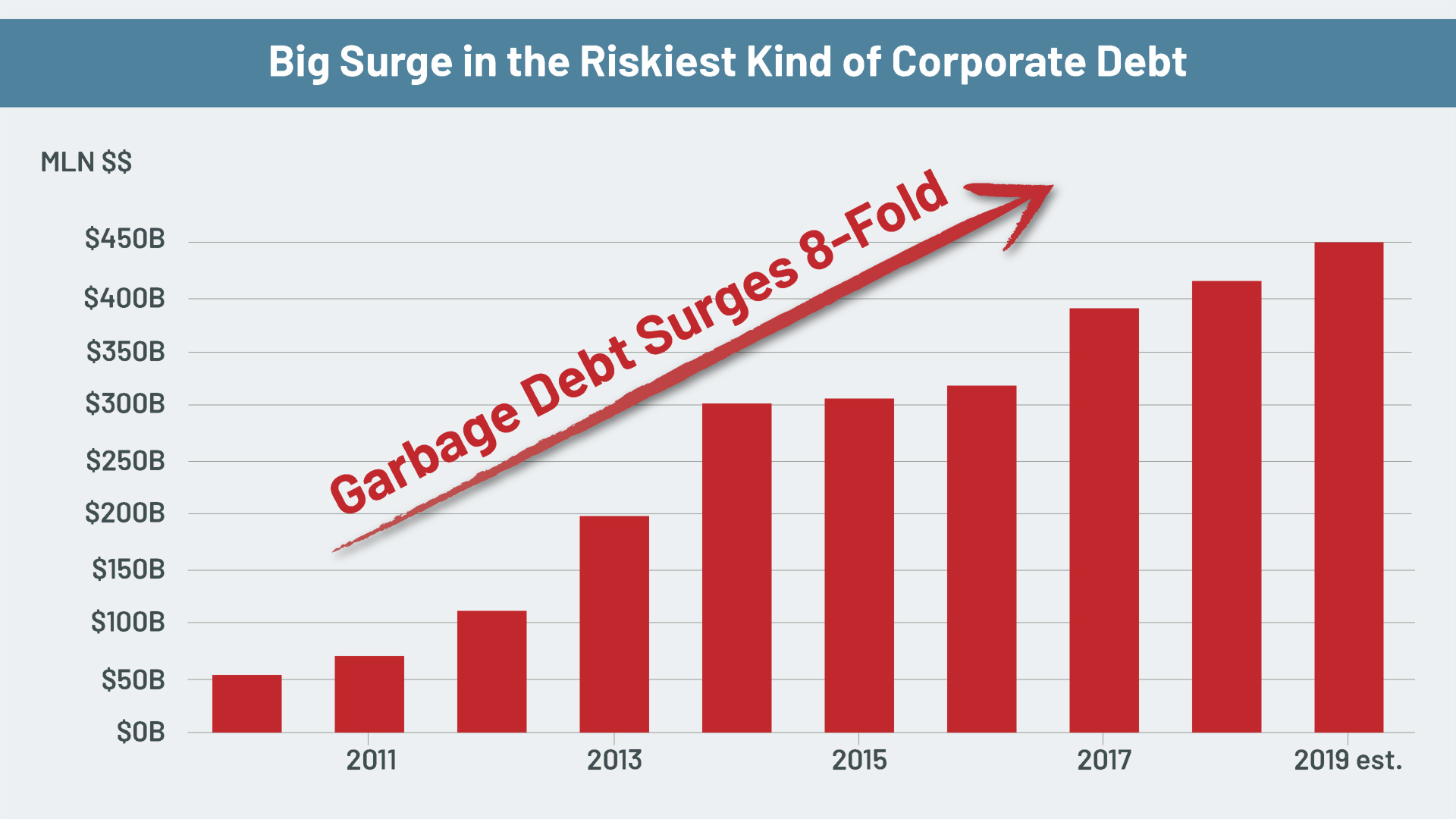

But since the last debt crisis, America’s companies have been piling up debt like there's no tomorrow — nearly $7 trillion worth!

And the biggest surge has been in the riskiest kind of corporate debt. These types of debts are called Covenant-Lite Loans, Covenant-Lite Loans.

Our senior analyst, Mike Larson, calls it “garbage debt.” And this garbage debt has surged roughly eight times since 2010 to an all-time record of nearly $400 billion.

In fact, the garbage debt now represents a whopping 75% of all leveraged loans, far and away the biggest market share of all time.

So …

There’s very little the government can do to make those financially sick companies healthy again.

And there’s nothing the government can do to prevent a plunge in corporate earnings.

They can’t stop companies from losing money. And that’s what’s already happening. All kinds of companies, giant oil companies, auto manufactures, airlines, hotel chains, restaurants, small family business. They’re losing money. Hand over fist.

There’s also nothing the government can do to stop companies from laying off millions of workers, and that’s also what we see happening. Everywhere.

There’s nothing the government can do to stop companies from canceling their stock dividends. And that’s what they’re doing: Huge companies like Ford Motor, Occidental Petroleum, Boeing, Delta, and Freeport-McMoRan. These are just a few of the many companies that have already slashed their dividends or have canceled them entirely.

And obviously, as we’ve already seen, there’s nothing the government can do to stop the stock market from falling.

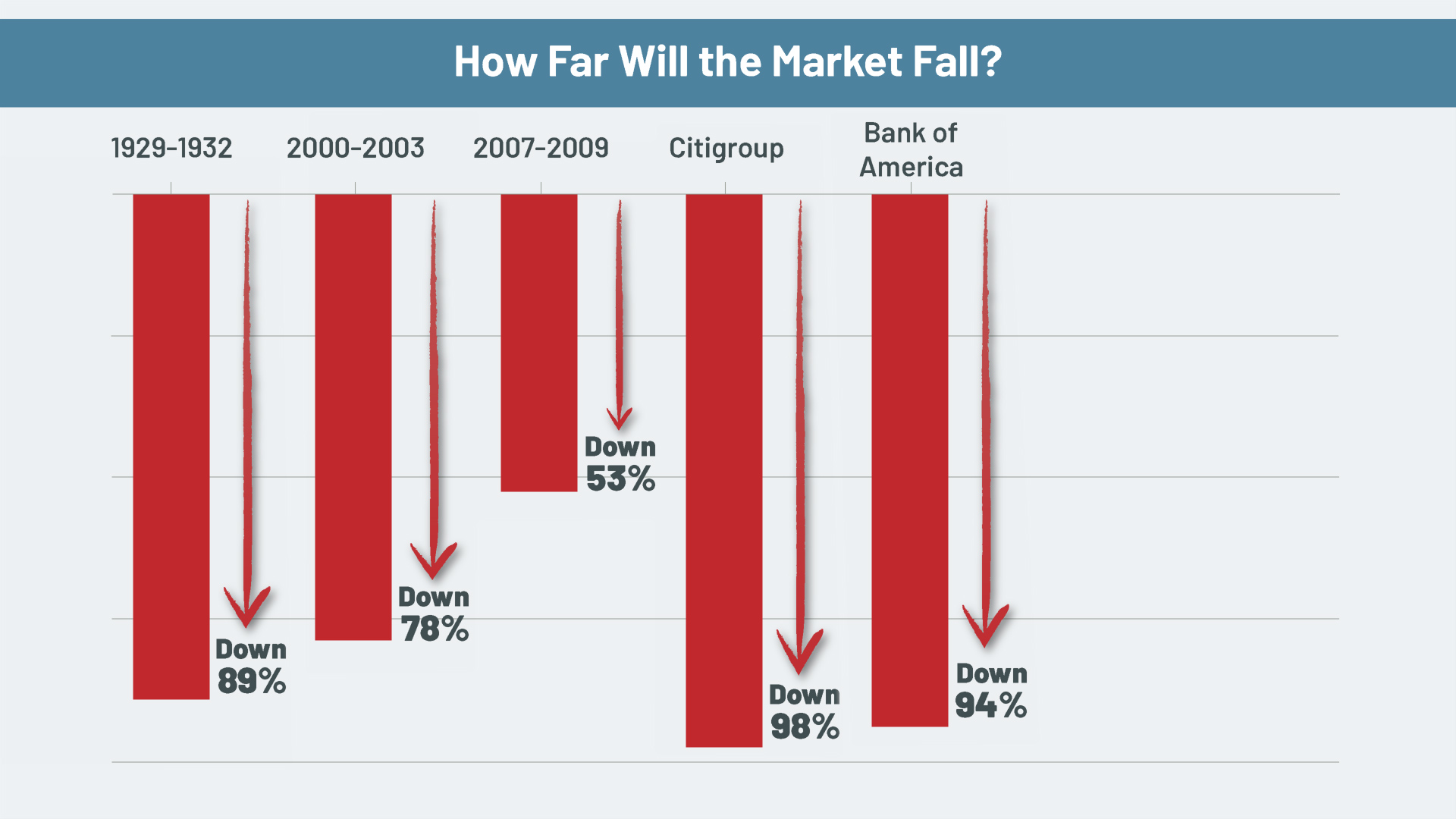

How far will the market fall?

Well, here’s the history …

- In the Crash of 1929 and the big decline that followed, the average stock in the Dow Jones Industrials fell 89% …

- In the early 2000s, the average stock in the Nasdaq Composite Index fell by 78%, and …

- In the 2008 Debt Crisis, the average stock in the S&P 500 fell 53%.

So that gives you some parameters of how much the average stock can go down in a crash: Anywhere from about half to as much as about nine-tenths.

That’s bad enough, right? But notice I said the “average” stock, and …

Not all stocks are average.

- In the early 2000s, a lot of supposedly great internet stocks lost 99%, even 100% of their value.

- In the 2008 debt crisis, shares in the largest bank in the United States, Citigroup, fell by 98%.

- Shares in the second largest, Bank of America, fell 94%.

These giant banks and other banks were on our endangered list many months before they failed, and anyone heeding our warning would have saved a fortune back then, another reason it's important for you to heed my warnings today.

Right now, if you have stocks or mutual funds, depending on what stocks you own and how this crisis unfolds, it's fair to assume that you could lose anywhere from half your money to almost all of your money.

Obviously, counting on the government to save your stock portfolio is not exactly a good strategy.

What about your real estate?

Again, there’s nothing the government can do to prevent your home from collapsing in value.

They tried desperately to stop home prices from plunging in 2008. But did that stop the housing collapse? No.

The average home fell by more than half, and in some markets, home prices fell a lot more.

Back in 2007, before the housing bust, the net worth of the typical American household was about $142,000. More than a decade later, even after a long so-called recovery, it was only about $56,000.

So, they were still down by 60% or so.

And that’s despite all the big government bailouts.

What about this time? Well, this time, the typical household could lose a similar amount or maybe even more.

But here’s the biggest problem of all, the problem almost everyone on Wall Street and in Congress seems to be ignoring:

The government has no money in

reserve, no savings whatsoever.

Instead, the government is running a huge deficit and it's deep in debt. Everybody knows that.

For the year 2020, even before all the big government spending to combat this crisis, the federal budget deficit was already going to be huge, more than $1 trillion. Everyone knows that, too.

But let me tell you now what nobody's talking about: Now, the federal deficit is going to be many times bigger.

Tax revenues have fallen apart. So that means a lot less money is coming into the government's coffers.

On top of that, the government is spending trillions of dollars to fight this crisis, right? So that's a ton of money going out of the government’s coffers.

All told, instead of a deficit of $1 trillion, which is already big, the deficit is going to be at least $4 trillion. It’s going to quadruple practically overnight.

I know that sounds unbelievable, but it’s true.

So, who is going to finance that deficit? And if this crisis gets a lot worse, who in the world would be able to bail out the government of the United States?

Don’t get me wrong, I’m not predicting that the U.S. government is going to default outright. I’m not predicting that the whole country is going to go bankrupt.

I’m just stating a fact of life, and it's the fact that you must always bear in mind:

There is LIMIT to how

much the government can do.

The government cannot bail out every small business and every big corporation in America.

It cannot bail out every city and state that's in trouble.

It cannot bail out all the banks that go broke.

So, you cannot, you must not, rely on the government to bail you out either.

Only you can truly protect your finances. You're the only one that can take your destiny into your own hands to save yourself and your family from financial disaster.

Even better, you can use our ratings to avoid

stocks that plunge and own the stocks that surge.

In the last crisis, for example, you could have used our ratings to avoid bank stocks that plunged as much as 99% while owning stocks that surged 102%, 103%, 115%, up to 120%.

And since 2007, if you had followed our stock ratings and our strategy for using them, you could have made a total return of 809%, including the period when the market was down.

That means you could have beaten Warren Buffett's Berkshire Hathaway by four to one. And you could have outperformed the S&P 500 by a whopping five to one.

This is important.

So, let me repeat what I said before: Our ratings not only can help you avoid big losses, they can also help you make money, even in the worst of times.

Let’s say that, in the last crisis, you heeded our forecast of banking collapses and bought a special kind of ETF, an exchange-traded fund, that goes up when bank stocks go down.’

- Between September 19th and November 21st of 2008, you could have made a gain of 144.1%. A $10,000 investment would have turned into $24,410.

- And during that same period, another investment designed to profit from the real estate decline posted a 354.9% gain, enough to more than quadruple your money. Your $10,000 would have grown to $45,490.

- Plus, as the crisis struck other industries, you could have used similar investments in other sectors to grab gains of 156%, 176%, 193%, 289%, and more.

Now, in this crisis, the profit

opportunities are even larger.

You can buy special investments to profit directly from a stock market crash. The faster and deeper the market falls, the more money you can make.

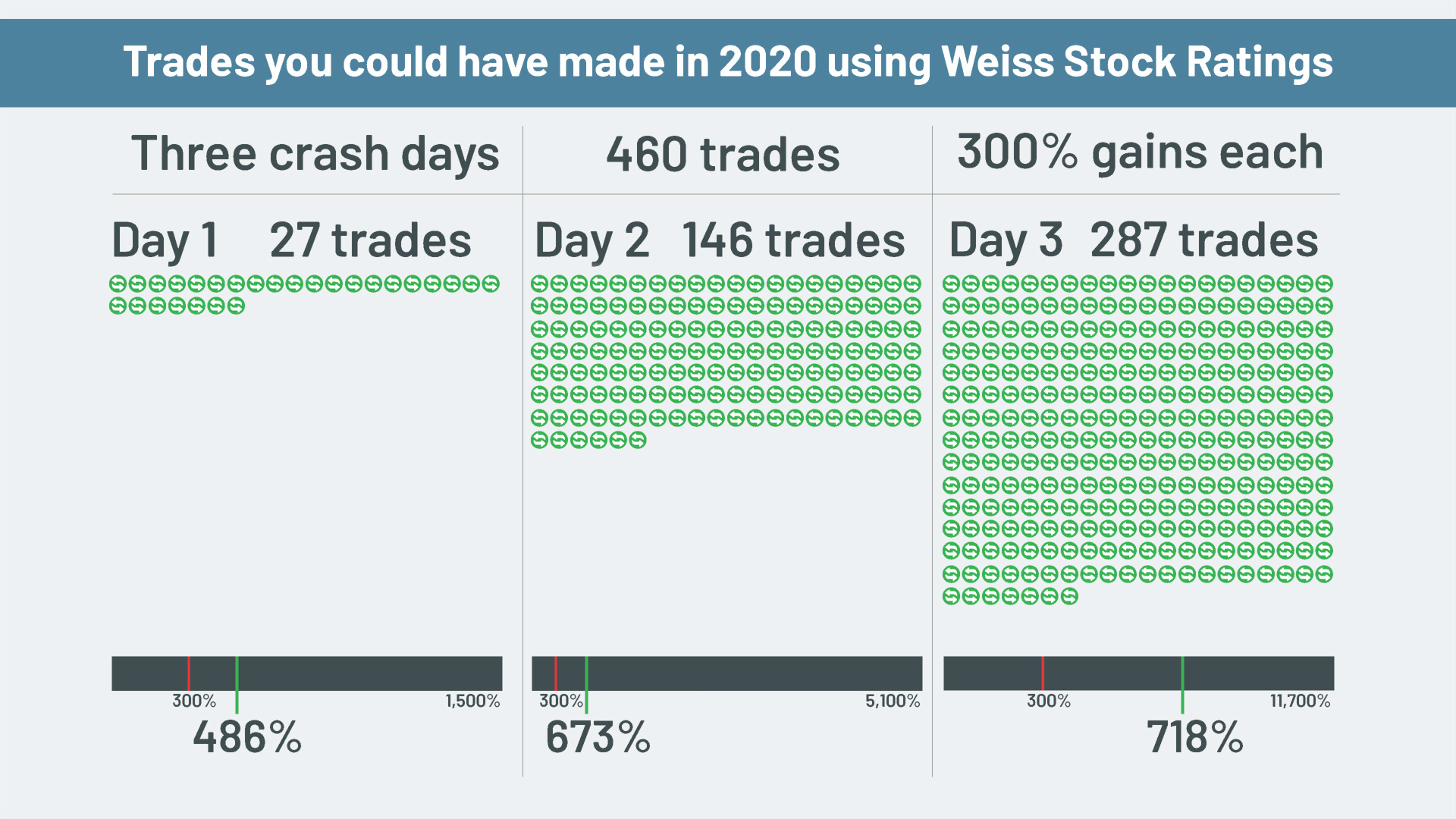

Just recently, for example, I looked at three separate days in the crash of 2020, and I counted 460 distinct trades selected by our Weiss Stock Ratings that could have made you at least 300% gains each.

- On the first crash day, we saw 27 trades that returned gains ranging from 300% to 1,500%. The average gain was 486%.

- On the second crash day, the numbers went parabolic: We saw 146 Weiss Ratings winners, ranging from 300% to 5,100%. Average gain: 673%.

- On the third crash day, it was even better: 287 winners, ranging from 300% to 11,700%. Average gain: 718%.

Even if you invested only $10,000, and even if you chose the least profitable of these trades, you could have made about $30,000 on the first day, $30,000 on the second day, and another $30,000-plus on the third day. That's a total of more than $90,000 in gains.

Or, if you invested those same $10,000 in just the average trades — not the best ones, mind you, just the average ones — you could have made $48,600 on day one, $67,300 on day two, and $71,800 on day three. That's a total of $187,700.

All without reinvesting profits. All in just three trading days.

And, of course, with more time, you could have made more money.

Now I want to warn you, any kind of investing involves risk, and that's equally true if you bet on the market going up, or you bet on the market going down.

But for a small amount of money you can afford to risk, you should consider it seriously for two reasons:

First, because of the tremendous profit potential I just told you about. It’s mind-boggling. While most other investors are losing their shirts and panicking about their future, you can be banking tens of thousands of dollars, giving you and your family the security you need.

Second, because it’s like buying “crash insurance.”

Let’s say you own stocks that are vulnerable to a crash, especially stocks that are on our endangered list.

And suppose you’re unwilling or unable to sell them. Maybe you have a stake in the company you work for and it’s not vested yet. Maybe the shares are in your pension plan or a family estate that you don’t control.

Plus, here’s another situation: a family business. Now, there are exceptions, but, for the most part, even if you wanted to, it would probably be very tough to sell your family business in the middle of this crisis.

So what do you do?

Well, this is where a hedge can be important. It’s like a firewall that you build around your assets.

You have assets that are falling in value in this crisis, right? So you buy investments that are designed to go up precisely when your other assets are going down.

That’s what I mean by a hedge. And that’s what those super-profitable trades can do for you.

You need those kinds of strategies. Not next year, not tomorrow, but today.

Look, I know that, even with everything going on today, the vast majority of Americans will fail to heed this warning and fail to get ready for the next phase of this crisis.

But I sincerely hope, for you and your family’s sake, that you’re not one of them. The precautions required to weather this storm are not difficult.

And even if the storm turns out to be less severe than we fear, the worst that’ll happen is that you’ll sleep better at night … and, potentially, you'll make some money in the process.

Because there is some good news:

First, as this crisis unfolds, the President, Congress and the Federal Reserve will continue to do absolutely everything in their power to pump up the economy. It won’t end the crisis, but it could trigger a temporary rally in the stock market. And that could give you a good chance to get out.

Second, at some point, the pandemic will peak and then subside. It won’t go away completely. But that too could be a trigger for a temporary recovery before the next decline.

So you should have some time to prepare — not much time, but some time.

Here are seven steps I recommend you begin taking immediately to protect yourself and your loved ones from the coming storm …

STEP 1

If you hold stocks or stock mutual funds in your …

- brokerage account

- 401(k), or

- IRA

Sell about HALF immediately, focusing on most vulnerable.

Step 1. If you hold stocks or stock mutual funds in your regular brokerage account, in your 401 or in your IRA, sell about half of your stocks immediately, focusing on the most vulnerable.

Which ones are the most vulnerable? Well, you can find out simply by checking the endangered list I send you.

STEP 2

Buy hedges!

Example — DOG

Step 2. But hedges!

There are many good ones to choose from, some more conservative, some more speculative.

Unless you're a very experienced investor, I don't recommend you buy the speculative ones on your own.

But here's one that can help you get started: It's DOG, D-O-G.

For every 10% decline in the Dow Jones Industrial Averages, this ETF, this exchange-traded fund, is designed to go up 10%.

STEP 3

Wait for a strong rally in the market. Then do this …

Step 3. Wait for a strong rally in the market. It could be getting underway right now. Or you may have to wait for the next one.

But, either way, use that rally as your opportunity to unload the rest of your vulnerable stock holdings.

STEP 4

Stash your cash in a truly SAFE place.

Step four is all about cash.

Even if it pays zero interest, don't underestimate the power of cash in a crisis like this.

You will need cash for safety, for emergencies, and later to pick up some amazing bargains on very valuable assets.

Right now, I have most of my cash in a Treasury-only money market fund. It buys exclusively short-term Treasury bills and equivalent. And I buy it online, right inside my regular brokerage account. Plus, some other brokers, probably yours, also offer something very similar.

Then, I'm moving some of my cash to what I call my "ultimate safe haven." It's an account I recently opened directly with the U.S. Treasury Department itself. You just hop online, you go to treasury.gov. And in less than 10 minutes, you can open a personal account or a corporate account.

I recommend you buy 13-week Treasury bills. Then just click on the box to automatically roll them over as they mature.

Now, okay, those are the basic steps.

Go to download page.

But there’s so much more I need to tell you to help you through this crisis, I couldn’t begin to cover it all in this presentation.

That’s why we’ve just put the finishing touches on a new report: “Second Wave of the Financial Pandemic: Your Guide to Financial Safety.”

In this indispensable emergency guide, based on nearly a century of experience in the markets going all the way back to the 1920s, we show you what to do immediately to protect your savings, your investments, your real estate and everything else you own.

We give you the keys to shield your bank account, safeguard your insurance policies and defend your 401(k) retirement account.

We give you specific instructions on how to insulate your stock portfolio, the value of your home and other real estate assets, no matter how bad things get.

Plus, you’ll learn how you could actually make money with investments that soar in a crisis like this.

STEP 5

Check the safety of your bank!

Go to download page.

Make sure your bank is NOT on our endangered list.

If it is, move your money to a stronger institution.

To help you identify them, I want you to have a complimentary copy of “The Weiss Ratings X List: America’s Weakest and Strongest Banks.”

In this guide, we give you the complete list of all the endangered banks and credit unions that you should avoid at all costs, and we also give you a full list of the strongest banks that are well-equipped to weather the next phase of this crisis.

STEP 6

Gold bullion bars and coins!

Go to download page.

Step 6. Own mankind’s greatest crisis hedge: GOLD!

Since we first began recommending them in 1999, gold bullion coins and gold bullion bars have risen by 450%. An initial investment of $10,000 is worth $55,000 today.

And that was before the financial pandemic we face right now.

So, we strongly recommend that you hold a modest portion of your liquid money in physical bullion, mostly smaller denomination bullion coins.

Did you know that you can actually get some free gold simply by selecting the right bullion coins to buy? It’s true.

And we’ll show you how in the third report we’ve prepared for you, “The Weiss Guide to Prudent Gold & Silver Investing.”

STEP 7

Stocks and ETFs:

Avoid the weakest and invest in the strongest.

Step 7. Avoid the weakest stocks now. And when we give you the signal, invest only in the very strongest stocks.

You know, one of the free services we are providing in this crisis is premium access to a powerful tool you can use to help decide precisely which ones they are.

And at a time like this, a powerful offense is your best defense.

Building up substantial profits that you can convert into cash reserves is the best way to ensure your family's safety and comfort.

Go to download page.

Plus, in your free copy of "America's Weakest and Strongest Stocks & ETFs," we introduce you to an entirely new way to invest, a way to keep your money growing safely no matter how rocky the political, social or financial situation becomes.

The data shows that, if you had used this strategy, you could have beaten the S&P 500 by five to one since 2007, with an overall return of 809%.

And I want to remind you, that period includes 2008, when stocks crashed.

That’s enough to turn $25,000 into more than $227,000, or $250,000 into nearly $2.3 million.

You don’t need a lot of money to start.

You don’t need to have a lot of experience as an investor.

And you don’t even need to use exotic investment vehicles.

You can download all four guides instantly so you can start using them just a few minutes from now.

Download all 4 free reports here.

- Second Wave of the Financial Pandemic: Your Guide to Financial Safety.

- The Weiss Ratings X LIST: America’s Weakest and Strongest Banks

- The Weiss Guide to Prudent Gold & Silver Investing, and

- America’s Weakest and Strongest Stocks & ETFs.

All I ask is that you apply for a one-year subscription to our flagship investment letter, Safe Money Report, for just a few cents per day.

You can cancel and receive a full refund at any time during your 12 months with us, including up to the last day of your subscription.

And, even if you decide to cancel, you can keep all four of the free guides that you download today.

I trust this time we've spent together has given you a lot of information you can use immediately.

And I look forward to welcoming you on board!

All the details are on this page.

Good luck and God bless!

Martin D. Weiss, Founder

Weiss Ratings