The Next Black Swans

To download your reports immediately, jump here.

Or, read on for the transcript …

Dear Investor,

America is in grave danger, extremely vulnerable to black swan events that strike out of the blue, that throw the world into turmoil, and that raise the specter of even darker black swans still to come.

Like the Russian invasion of Ukraine, decimating an independent democracy larger than Germany and the UK combined, reducing its cities to rubble, sending shock waves through the global economy.

Or a massive future air attack on the independent democracy of Taiwan, igniting a new war in the South China Sea, spreading to the entire Pacific region, plunging East-West trade into turmoil.

How much damage could just one of these black swans cause?

For an answer, let’s not forget the black swans that have struck our nation since the beginning of the new millennium:

The black swan that attacked the very heart of our nation on 9-11 with great loss of life and treasure, setting off a chain reaction of events that have continued to ricochet through time:

The U.S. invasion of Iraq, the fall of Saddam Hussein, the rise of Al Qaeda, the global spread of the Islamic state, and then ...

Billions of dollars in new money printing by the U.S. Federal Reserve.

Or the black swan that attacked the very heart of our economy.

It wasn’t September 11th, 2001.

It was September 15th, 2008 — the Lehman Brothers failure, again, setting off a chain reaction of events that have continued to ricochet through time:

America’s deepest recession since the 1930s.

America’s largest bank failures and bailouts of all time. And then ...

A massive wave of central bank money printing that was many times larger than anything we’d ever seen before.

If you missed any part of this video or want to see it again, click here.

Or like the black swan virus that suddenly burst onto the scene, spread rapidly around the globe and mutated into even more contagious strains, transforming our cities into ghost towns, plunging financial markets into a tailspin, prompting governments to lurch from inaction to reaction, and then ...

Driving the Fed to unleash a tsunami of money printing that makes all prior money-printing binges look tiny by comparison.

I am not here to frighten you.

God knows, there’s enough fear in the world today. I’m here to give you the facts about the threats to your wealth so you find safety in an unsafe world.

Now, maybe you’re thinking that, once the world calms down and global conflicts recede, the inflation and economic turmoil will end, too.

If I were you, I wouldn’t bet on that either.

Long before the latest black swan events, we already had all the ingredients of a serious financial crisis here in America.

In fact, seeds for this crisis were planted a long time ago with …

More than two decades of Federal Reserve money printing …

Years of bad advice from Wall Street …

Dishonest ratings — and lies — that lured millions of people into debt …

That spurred millions of investors to throw caution to the wind …

That drove nearly everyone to take unprecedented risks with their hard-earned money.

If you find that hard to believe, I’ll give you the evidence here. I’ll show why we believe thousands of companies and even many banks are unprepared for the next black swans.

I’ll tell how many we identified were already in deep trouble before this latest phase of the crisis began.

And, before you and I part today I will give you access to my family’s — and my company’s — most precious crisis-investing guidance.

Because right now, the black swan events — along with the government’s reactions to the black swans — are creating three threats to investors.

Threat #1 is the destruction of any

decent interest you could possibly

earn on your savings.

Just look at what the Federal Reserve has already done:

The Fed has printed so much money, it has repeatedly wiped out any decent yield investors can earn without taking crazy risks. Now, adding insult to injury, the resulting inflation is decimating their principal as well. For our solution, go here.

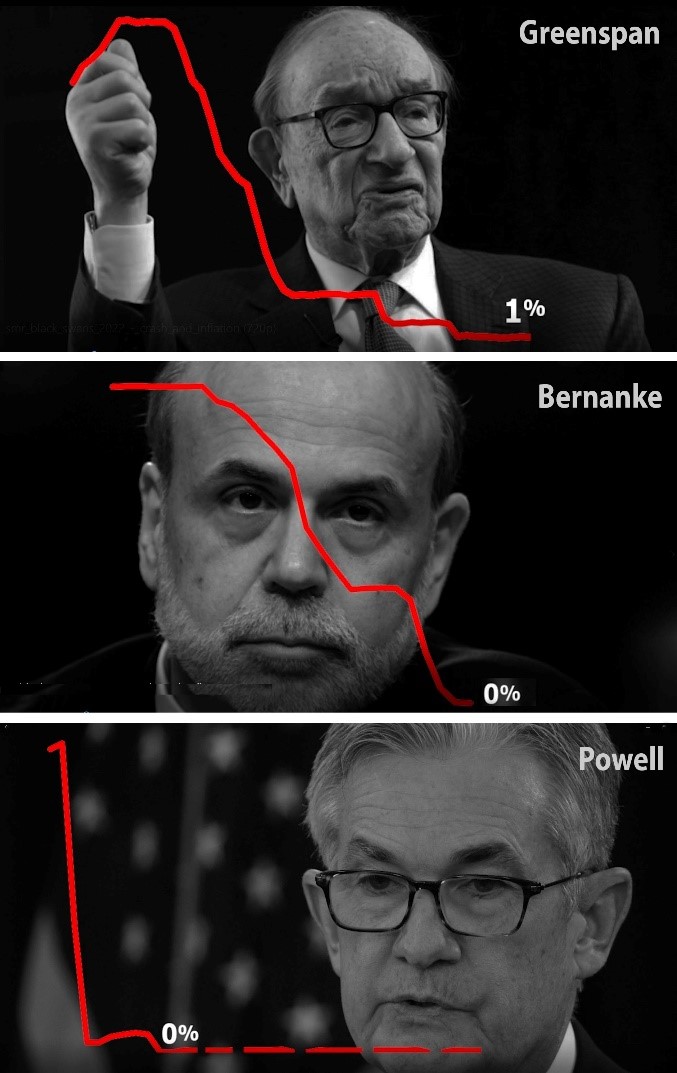

In response to the first black swan of the millennium, the 9-11 attacks, Federal Reserve Chairman Greenspan drove the Fed’s key interest rates down to 1%, gutting the yield of income investors.

In response to the second black swan, the Lehman Brothers failure, the next Fed Chairman, Ben Bernanke, drove rates down to zero, wiping out the yield of income investors. And...

In response to the third black swan, Covid-19, Fed Chairman Powell not only slammed interest rates down to zero, he kept them near zero for two full years, nearly obliterating people’s income today and for years to come.

What’s the solution?

In this session today, I’ll tell you about an investment strategy that generates about $1,000 in extra income per week with 98% accuracy. And with double the investment, about $2,000 per week.

Threat #2 is the rapid erosion of

your PRINCIPAL by out-of-control inflation.

This is no longer just a prediction. Inflation is already surging.

And the rising tide of conflict in the world today can only make it worse.

Not just wars in one country, not just wars in one region, but also trade wars, cyberwars and massive supply-chain disruptions all over the world.

I know. The inflation we’re seeing now is shocking. But what’s even more shocking to me is that most people are still so complacent about the truly dangerous inflation that’s rearing its ugly head today.

They didn’t live through the 1970s, when folks waited in gas lines for long hours just to top off their tanks … when the value of supposedly ultrasafe Treasury bonds plunged by more than half and … when the price of gold surged 2,324%.

To avoid the dangers and start reaping the great rewards, click this link.

They didn’t live through the inflation that gutted the economy of Brazil in the 1970s and Argentina in the 1980 … destroying the savings of millions of middle-class citizens … bankrupting their governments … prompting their leaders to confiscate their bank accounts … unleashing mass protests against inflation, and …tearing apart the fabric of society.

Nor does anyone dare think about the hyperinflation that wreaked havoc on the entire world …

Starting in Germany after World War I …

Creating the greatest avalanche of worthless paper money ever seen, and …

Giving rise to the most murderous dictator in the history of Western Civilization.

Hundreds of millions of Americans going about their daily business in America today are oblivious to the torrid past of inflation.

Fewer still believe anything vaguely similar might be possible today.

They have not yet learned the lessons of history.

And they don’t yet see the handwriting on the wall:

The consequence of complacency is catastrophe.

The solution is investments that have historically demonstrated a consistent pattern of surging when inflation rises and skyrocketing when inflation surges.

I’ll offer you specific insights on our selection of some the best in just a moment.

Threat #3 is the next great crash,

one of the most damaging black swans of all.

What’s the trigger? For an answer, just look at what the folks at the Fed have done.

They pushed interest rates down to practically zero. They encouraged everyone to borrow like drunken sailors. They pushed investors into the highest-risk stocks in the market. And they created some of the biggest speculative bubbles of all time.

So what happens when the Fed raises interest rates and takes away all that cheap money?

Well, it’s obviously too little, too late to stop the inflation. But it’s also too much, too soon for the stock market.

The Fed pop the bubbles. And the stock market comes crashing down.

I know. Because my family and I have lived through market crashes and even predicted them ahead of time.

The story begins with my father, Irving Weiss, who first went to work on Wall Street in the late 1920s as a Customer’s Man, which nowadays they’d call a stockbroker.

The stock market of the 1920s would be eerily familiar to anyone who has lived through the current crisis. It was enjoying a roaring bull market that was unusually long, just like it has been doing in recent years.

And the market was unusually out of sync with the tough times that most working American families were experiencing, also much like recent years.

So, when the Dow Jones Industrials kept going up in the first ten months of 1929, my father didn’t trust it.

He didn’t trust the disconnect between the great times on Wall Street and the tough times in the neighborhood where he lived.

He didn’t have many clients yet — just friends and family. But he told them to get the heck out of the market.

In his office, the veteran stockbrokers laughed at him. “Weiss is just a kid,” they said. “What does he know?”

And then came Black Monday, October 28th, 1929. The market plunged the equivalent of about 4,500 points in the Dow Jones of today.

On the next day, it plunged the equivalent of another 4,000 points.

It was like an 8,500-point crash in just 48 hours.

Suddenly, Irving was a hero, and suddenly the word got around that he was the only one who saw it coming.

That’s when he decided to do more, much more.

He collected data on as many companies as he could. He put the numbers down on the large, green sheets that bookkeepers used, spreadsheets actually. And he created a series of formulas that would later become the foundation my company’s own computer models of today.

Using his formulas, he identified the companies that he thought were the riskiest. He called them “Dogs of the Dow.”

Then, in April of 1930, after a big stock market rally, Irving borrowed $500 from his mother, and he started selling short the Dogs of the Dow. When the market plunged, he took profits. Whenever it rallied, he shorted again.

By the time the Dow hit rock bottom in 1932, he had over $100,000, or nearly $2 million in today's money. That was about 200 times his money.

Not bad for a young man who was just a rookie on Wall Street, right?

Are there ways for investors to do something similar in today’s market? Absolutely! But save that thought for a moment.

In the early 1930s, Dad also used his formulas to identify the strongest companies in the market, like gold mining companies, for example.

Years later, he wrote …

“In those days, very few people were buying the gold, which was ironic because you could buy it so easily. All my clients and I had to do was go to our bank, walk up to the teller window and ask for $20 gold coins. And that’s what we did.”

So, he figured he couldn’t go wrong if he concentrated on the companies with his highest grades, like Homestake Mining Company and Dome Mines Limited.

Most investors today have no idea how large the profits were in gold shares in the 1930s.

Homestake rose from $65 per share to $130 and change in 1931. Then it doubled and doubled again to more than $540 a share in 1936.

In the meantime, Homestake’s dividends also doubled and redoubled, reaching $56 per share in 1935.

Think about that:

The dividends earned in one year

alone almost paid back the entire

purchase price of the stock.

Dome, another great gold producer, did even better. You could have bought Dome for as little as $6 a share and sold them for $61 a share.

A person who put $10,000 into Dome could have walked away with more than $100,000, excluding dividends.

Is it possible that history will repeat itself? Everything I see happening today tells me the answer is yes. And it all comes back to one of the last predictions my father made before he passed away.

He warned that, someday, the stock market will crash again. He didn’t say exactly when it might happen, but he did tell me how it would happen.

“Inflation will run amuck, and the Fed will try to fight it with higher interest rates. That’s when the stock market will crash, and the Fed will start printing money again.

"But the crisis will be so severe, all the government’s money printing and all the government’s spending will still not be enough to put things back together again.”

Now that crisis has begun. And now, we can see clearly how all the threats could soon converge in one time and place.

The utter destruction of any interest you could safely earn on your money.

The rapid erosion of your principal with raging inflation.

And the growing risk that your stock portfolio could also be gutted.

Not to mention wars and the threat of new wars.

This is a very solemn moment in history — a time for prayer, but also a time for action.

And a few minutes from now, I will give you our roadmap for six steps to take starting immediately — to protect everything you have. Your stocks and mutual funds, your 401k and IRA, your real estate and your savings.

Plus, with these steps, investors could also turn this crisis into an opportunity to swiftly build your wealth.

This is urgent, because this is no ordinary financial crisis.

It's far bigger than anything we've ever experienced in our lifetime, and it's striking with far greater speed. Almost everything you own is in jeopardy, even things that you thought would be safe.

Not just money you have in stocks, but also money you have in bonds and even banks.

Not just right now, but for many months to come.

All of those assets are tied to the fate of the economy.

Even if this crisis does not turn out to be as bad as we fear, investors could still lose half of their money, and in many situations, they could even lose all I’ll explain why in a moment.

One half century ago, I founded my own company, Weiss Ratings, to help Americans of all walks of life keep their money safe — in good times and in bad times as well.

We transformed my father’s spreadsheets and formulas into a massive database on more than 56,000 companies and investments — stocks, ETFs, mutual funds, banks, insurance companies, even thousands of digital assets.

And today, that entire database has been modernized by a team of analysts, mathematicians and data scientists, using our advanced computer models to identify the weakest and the strongest every day of the year.

That’s how we warned in advance about the Dot-Com bust of the early 2000s and the great Debt Crisis of 2008. But …

We don’t just issue warnings.

We also issue RATINGS,

the Weiss ratings!

We provide a letter grade from A to E on nearly every stock, every ETF, every mutual fund and every financial institution in America.

With those ratings, we NAME the stocks that are likely to fall the most.

We NAME the banks that are most likely to go bankrupt.

Before the Debt Crisis of 2008, for example, we warned about nearly every major institution that failed and we did so months in advance.

We named Lehman Brothers as a candidate for failure 182 days before it went bankrupt.

We named Fannie Mae over one year in advance, Citibank, Wachovia Bank, and Washington Mutual Bank 51 days in advance … General Motors five months in advance, and many more. Among the 465 banks that failed during and after the debt crisis, we warned consumers about 464.

Yeah, we missed one, but that was only because the bank had committed fraud — it fraudulently kept hidden from everyone.

These kinds of on-target warnings prompted Worth magazine to say that our “record is so good compared with that of our competitors ... consumers need look no further.”

And The New York Times to say we were “the first to see the dangers and say so unambiguously.”

Barron’s wrote, Weiss is “the leader in identifying vulnerable companies.”

Chris Ruddy, founder of Newsmax and a close friend of former President Trump, said our “prediction of the current economic crisis is uncanny.”

And Louis Rukeyser of Wall Street Week wrote that we provide “a tougher service.”

And, I want to tell you that the service he was referring to includes a very important list of companies that, based on our ratings, are at the gravest danger. We call it the ENDANGERED LIST.

But I must warn you. Our endangered list is very long, and that’s the best evidence I can give you that the threat to your wealth could be deep and long-lasting.

Even before this phase of the crisis began, our endangered list included:

* Over 7,000 stocks, ETFs and mutual funds.

* More than 1,000 banks and credit unions with insufficient capital to withstand an ordinary recession.

* Plus another 3,000 that were unprepared for the next black swans.

And now, I’m sad to say, our endangered list is getting even longer.

So, the probability is high — and getting higher — that, if you’re an average investor, many of your stocks and mutual funds and even your bank could be on the endangered list.

Not all companies are in bad financial shape, mind you. There are still strong ones, and I’ll tell you about those in a moment.

But whether good or bad, you just need to know. And you need to know NOW, before the next black swans strike America.

Plus, there’s one more thing I want you to know.

Until now, we charged a fee for folks to access our ratings. You see, we’re not like Standard & Poor’s, Moody’s, and Fitch.

Because when they issue a rating on a company, they get paid by that company for the rating. Their ratings are bought and paid for by the rated companies.

Many smart people think that’s a serious conflict of interest, and I agree. Plus, it’s also one of the reasons why millions of people who followed their ratings lost so much money in the Great Debt Crisis of 2008. We never do business that way.

We have never taken a dime and never will take a dime from the companies we rate.

Our only source of revenue is the end user of our information, average people who want to get safe and make some money, too. But because of this crisis …

I don’t want any barriers between our ratings and your safety.

So, for the duration of the crisis, I propose to give you access to all of our ratings lists for free.

Look, I know that the vast majority of Americans will fail to heed my warnings and fail to get ready for the next black swans.

But I sincerely hope — for you and your family’s sake — that you’re not one of them.

The precautions required to protect yourself from the next black swans are not difficult. Even if the storm they create turns out to be less severe than we fear, the worst that will happen is that you’ll sleep better at night.

And potentially make some good money, too.

Because there IS some good news: You have some time to prepare.

But not much time.

Here are the six steps I recommend you begin taking immediately to protect yourself and your loved ones from the storm I see coming ...

STEP 1

Avoid the Endangered Stocks

If you hold stocks or stock mutual funds — in your regular brokerage account, in your 401(k) or in your IRA — start selling the ones we’ve identified as the most vulnerable to the next black swans.

In the market decline during the Great Debt Crisis, for example, investors could have used our ratings to avoid 385 stocks that fell 90% or more in value. And on average, the stocks that were on our endangered list when the crisis began lost more than two-thirds of their value.

To download this report now, click here for all the details.

This time around, the most vulnerable are different names in different sectors. But you can find out exactly which ones they are simply by checking our special bonus report, The Weiss Ratings Endangered List.

In it, I give you a complete list of all the stocks, ETFs, and mutual funds with our lowest ratings — investments I wouldn’t touch with a ten-foot pole.

STEP 2

Learn How to Earn $1,000 in Income Per Week.

By income, I mean cash flow into your brokerage account.

Imagine an investment strategy that has generated about $1,000 in extra cash flow almost every Friday.

That could add up to $50,000 per year.

And with double the investment, could add up to $100,000 per year.

To download this report now, click here for all the details.

Imagine a success rate of 98% on your trades.

Well, you don’t have to just imagine anymore. Because we feel it’s an appropriate solution to overcome the terrible low yields that continue to plague the financial world.

Our Safe Money Report editor, Mike Larson explains exactly how in his special report, Instant Income Revealed.

STEP 3

Own Mankind’s Most

Traditional Crisis Hedge: Gold.

Since my family began recommending $20 gold coins in the early 1930s, the price of gold has risen 9,595%.

Better yet, if some of my father’s clients bought one of my father’s favorite gold coins at the time, the St. Gaudens $20 gold coin, and their family kept in good condition until today, they could have seen it appreciate to an estimated $42,000. From $20 to $42,000.

That’s a gain of 206,288%.

Now, I’m not saying you can make that much money in gold this time around. Nor am I expecting you to wait 90 years for that to happen.

But in more recent years, since Weiss Ratings began recommending gold bullion coins and bars in our monthly newsletter, gold has risen by 459%. An initial investment of $10,000 is worth $55,000 today.

To download this report now, click here for all the details.

We show all the ins and outs of precious metals investing in our third bonus report we've prepared for you — The Weiss Guide to Prudent Gold & Silver Investing.

STEP 4

Learn How to Profit Directly from Market Declines.

How far could the market fall? Well, here’s the history …

In the Crash of 1929 and the big decline that followed, the average stock in the Dow Jones Industrials fell 89%.

In the early 2000s, the average stock in the Nasdaq Composite Index fell by 78%.

And in the 2008 Debt Crisis, the average stock in the S&P 500 fell 53%.

So, that gives you some parameters of how much the average stock can go down in a crash: Anywhere from about half to as much as about nine-tenths.

That’s bad enough, right? But notice I said the “average” stock, and not all stocks are average.

In the early 2000s, a lot of supposedly great internet stocks lost 99%, even 100% of their value.

In the 2008 debt crisis, shares in the largest bank in the United States, Citigroup, fell by 98%.

Shares in the second largest, Bank of America, fell 94%.

These giant banks and other banks were on our endangered list many months before they failed, and anyone heeding our warning would have saved a fortune back then, another reason it's important for you to heed my warnings today.

Right now, if you have stocks or mutual funds, depending on which stocks you own and how this crisis unfolds, it's fair to assume that investors could lose anywhere from half your money to almost all of their money.

The good news is that you can buy special investments to profit directly from a stock market crash. The faster and deeper the market falls, the more money investors stand to make.

Let me give you some salient examples.

During the Great Debt Crisis, the S&P 500 fell by more than half and nearly all investors lost fortunes. But there was also a minority of investors who owned ETFs designed to profit from the crash, called inverse ETFs.

My team surveyed all 24 of the inverse ETFs available to U.S. investors at that time and we calculated the gains on each.

Among the 24 ETFs, 14 went up by 100% or more, giving investors gains of 103%, 110%, 124%, 134%, 147%, 150%, 157%, 163%, 168%, 174%, 195%, 198%, 243%, 293%.

In addition, seven of the ETFs went up by 70% or more, giving investors gains of 73%, 73%, 84%, 89%, 90%, 92% and 96%.

On average, these ETFs went up 126%. And not a single one lost money during that period.

Investors could also have made a lot of money with inverse ETFs during the Covid Crash of 2020, and by that time, there were many more to choose from.

We counted 88 in all.

Among them 76 were winners with an average gain of 102% each.

And 12 were losers with an average decline of 20%.

The average gain overall was 86%. All in just 33 days! All while nearly everyone else in the market was losing money hand over fist!

But if you think those kinds of gains could be a good defense against a stock market crash, wait till you see how much money can be made with options.

Back in the early 1930s, my father had no access to put options. So he had to go short stocks outright, which exposed him to unlimited risk. “Whenever the market was turning against me,” he said, “I was sweating bullets. I could have lost a lot more than I invested.”

Today, however, thousands of different put options are traded in large volume and are widely available to average investors.

With the purchase of options, you CAN lose all the money invested, but … never a penny more. So, your risk is strictly limited to the amounts.

Provided you don’t over-invest, I think they’re cheap insurance. And they can also be used to MAKE a lot of money in a falling market.

For example, we looked at three separate crash days in 2022. Then, among the S&P 500 stocks that did not get good Weiss Ratings, we identified sixty two trades that could have produced gains of at least 300%.

On the first crash day, we identified 27 trades that returned gains ranging from 100% to 419%. The average gain among them was 206%.

On the second crash day, the numbers were better: We saw 19 trades with gains ranging from 100% to 809%. Average gain: 251%.

On the third crash day, it was even better than that: 16 trades ranging from 100% to 1,130%. Average gain: 324%.

There were also lots of trades that produced less than 100% gains. But even if you include all trades in all three days, the average return was 110% on day one, 101% on day two and 149% on day three. That’s an average of 120% gains per day.

All with investments that never expose you to unlimited risk. All without reinvesting profits. All in just three trading days.

So, that gives you two instruments designed especially for protection and profit in down markets. Put options which are ideal for crash days in the market, and inverse ETFs which I think are ideal for down markets overall.

If you hold almost any kind of vulnerable asset, you may need the kind of hedge that they can provide.

For example, suppose you own stocks, real estate or even a family business that could suffer a big decline. And suppose you don’t want to sell them … or you can’t sell them because they’re locked up in a trust … or because it’s hard to find buyers.

To download this report now, click here for all the details.

What do you do? Well, that’s when you can use inverse ETFs or even put options as a hedge. While your vulnerable assets are going down, the idea is that at least these hedges will be going up. And in a world that’s now more vulnerable than ever to black swan events, I think many investors may NEED that kind of protection.

Before you jump into them, I strongly recommend you read our guide: Crash Profits: How to Protect Your Portfolio in Down Markets.

STEP 5

Own companies that have historically

done very well in times of high inflation.

To download this report now, click here for all the details.

I’m referring to companies that mine natural resources or that build their business around some of the most powerful inflation hedges of this era.

We name them in our special report The World’s Leading Resource Companies.

STEP 6

Stay up to Date With

Our 56,000 Different Ratings.

One of the free services we’re providing in this crisis is premium access to all our ratings. One half century ago, I founded my own company, Weiss Ratings, to help Americans of all walks of life keep their money safe — in good times and in bad times as well.

- 10,000 common stocks

- 2,400 Exchange-Traded Funds (ETFs)

- 26,000 mutual funds and

- 1,600 cryptocurrencies.

Plus, you not only get full access to all of our investment ratings, but you also get full access to all of our safety ratings on …

- 4,800 banks

- 5,000 credit unions, and

- 3,600 insurance companies.

That gives you the power to select, at will and at any time, the ones to avoid and the ones to favor for the best combination of relative safety and profit potential.

Both when the market soars and when the market sinks!

At a time like this, a powerful offense is your best defense. Building up substantial profits that you can convert into cash reserves is the best way to ensure your family’s safety and comfort.

You don’t need to have a lot of experience as an investor.

And you don’t even need to use exotic investment vehicles.

In a moment, I’ll show you how to download and access the bonus reports instantly — so you can start using them just a few minutes from now!

The Weiss Ratings Endangered Lists

Instant Income Revealed

The Weiss Guide to Prudent Gold & Silver Investing

Crash Profits: How to Protect Your Portfolio in Down Markets

The World’s Leading Resource Companies

Not to mention premium access to the 56,000 Weiss ratings!

You get all of this right now. All I ask is that you apply for a one-year subscription to our flagship investment letter, Safe Money Report for just a few cents per day.

You can cancel and receive a full refund at any time during your 12 months with us, including up to the last day of your subscription. And even if you decide to cancel, you can keep all of the guides, reports and ratings information you download today or that you download at any time during the course of the year.

Fortunately, a small minority of investors WILL escape the dangers and even use this crisis to build substantial wealth. And if you act promptly on the simple steps I’ve given you today, you could be one of them.

You cannot rely on the government or anyone else to come to the rescue. Only you can protect yourself and your family. Only you can take your destiny into your own hands to create a better world for yourself.

I trust this time we’ve spent together has already given you some of the information you need to make that possible.

And I look forward to welcoming you on board to guide you the rest of the way. Click here for all the details.

Good luck and God bless!

Martin D. Weiss, PhD

Weiss Ratings Founder