America’s Day of Reckoning Has Begun

- How to find safety in an unsafe world.

- How to go for rapid profits in bad times.

- Avg. gain in recent crashes: 120% per DAY!

Chapter 1

The Stark Reality of Our Times Has a Profitable Silver Lining

As I write these words today, double-digit inflation is already in the cards and the America’s Day of Reckoning has barely begun.

But most investors continue to ignore the dangers.

They think the only time they can make money is in good times.

They don’t realize that some of the biggest profits can be made in the worst of times.

So, they grasp at any good news they possibly can.

They hear some random news about the economy recovering.

They hear news that the government plans to fight inflation and prevent a recession.

And they rush to buy stocks.

This helps bring about what I call “sucker rallies” in the market, luring investors deeper into a great trap.

And again, most investors fail to realize that, instead of getting sucked in …

They can use stock market rallies to buy special investments that could be extremely profitable in the big declines that will follow.

Why do I predict the market will fall again?

Because the Fed has no choice but to raise interest rates faster than investors expect. And because even after they raise interest rates, they will remain FAR behind the curve in tackling inflation.

The silver lining: If you follow the simple steps I recommend in this ebook, not only can you protect your wealth from the ravages of this crisis, but you can also make the best of this crisis to build wealth swiftly.

The strategy you’re about to discover can help you turn this crisis in your favor. In fact, it has already shown us waves of massive gains were possible. The list includes 416% on Intuitive Surgical, 525% on Bed Bath & Beyond, 1,700% on NIO Limited and many more. All in a single day. (Average, including all trades reviewed: 120%.)

Click here if you want to jump to my chapter dedicated to this topic.

All these events are unfolding with great speed. So, to adapt, we also need to act with great speed.

In this e-book, I alert you to what I predict will be the some of the biggest dangers — and biggest profit opportunities — in a lifetime.

I will show you how you can learn about them well in advance.

I will name the specific investments investors can buy to go for profits in the next decline … and then go for profits again when a true recovery gets under way.

But let’s face the facts. You and I cannot count on the government to stop inflation from raging or prevent a stock market crash.

This is the time to take your destiny into your own hands, and in the chapters that follow, I show you how.

It starts by taking a few, simple but powerful steps to protect yourself, right now.

Almost everything people own could be in jeopardy, even things thought to be safe — not just money in stocks, but also money in bonds and banks; not just right now, but for many months to come.

Chapter 2

The Next Phase of the Collapse Revealed: What’s Coming Now and How To Prepare

Some people seem to think rampant inflation is not a real concern, or even that this crisis is nearing an end.

Some folks even claim that the bear market is already behind us, and they’re loading up for “the next 10-year rally.”

Don’t make that mistake.

Everything is telling us that the crisis is just starting, and the next shoe is about to fall: A worldwide recession, followed by a tsunami of defaults and bankruptcies.

Tens of millions of Americans will default on their mortgages, on their auto loans and on their credit card payments.

Businesses, whether big or small, will do the same thing.

It will create a chain reaction: Finance companies will default on their obligations to their creditors. And hundreds of banks, especially those on our endangered list, will go bankrupt.

Corporate dominoes in Europe and Japan will fall at around the same time. And in emerging markets, as supply-chain disruptions disrupt their economies, the bankruptcies will be even more widespread.

A lot of people and a lot of corporate executives are counting on the government to save them. But if I were you, I wouldn’t bet on it.

Sure, the government can bail out some companies and some banks some of the time. But can the government bail out everyone all of the time? I’ll answer that question in Chapter 4.

But here’s the big question: If the U.S. government spends too much money to bail out everyone else, who will bail out the U.S. government itself?

Already, one thing is abundantly clear: No matter what the government has done, or plans to do, the inflation we’ve seen so far is already the worst in more than 40 years. And the impact on the economy has barely begun.

When the dust settles, I predict the collapse of 2022 will ruin the American dream for millions. And for most American families, nothing will ever be the same again.

I don’t want that for you.

Now, maybe you’re thinking: Once inflation settles down, then the financial crisis will end, too.

I wouldn’t bet on that either.

The reason is important. So, I want to underscore here: Before this scorching inflation appeared, we already had all the ingredients of a serious financial crisis in America.

In fact, this crisis actually began a long time ago with years of government manipulations, bad advice, dishonest financial ratings and even outright lies.

But it’s the Federal Reserve’s actions over the last 12 years that have really put America in a great bind — over $8 trillion in newly printed paper money, the true cause of the inflation that’s now rearing its ugly head.

It was the Fed’s monster $8 trillion money printing that encouraged Main Street and Wall Street to take on so much debt. It was the Fed that spurred millions of investors to throw caution to the wind. It was the Fed that drove nearly everyone to take unprecedented risks with their hard-earned money.

And now, the United States of America has a massive $57 trillion debt mountain that is about to implode, threatening a far more damaging downturn than what we saw in the Great Debt Crisis of 2008, when the economy almost collapsed on itself.

If you find that hard to believe, I understand. I’ll give you the evidence in a moment. I’ll show you how most people, most companies, even most banks in America are unprepared for this crisis.

I’ll tell you exactly how many of them were already in deep trouble before the crisis began.

And I’ll explain why I predict many will not survive.

But fortunately, a small minority of investors will escape the dangers and even use this crisis to build substantial wealth. If you act promptly on the simple recommendations I provide in this ebook, you could be one of them.

How? It starts by understanding the danger that could be lurking inside your current portfolio.

Chapter 3

How You Can Learn about the

Dangers and Opportunities

Ahead of Time

Over 50 years ago, I started my own rating and research company, the successor of my father’s company, which he started decades before that.

How Irving Weiss Made 200x His Money in the Great Bear Market of 1929-1932

Irving Weiss Circa 1928

Martin’s father, Irving Weiss, collected data on as many companies as he could and created a series of formulas (the precursor of the Weiss Stock Ratings) to identify the “Dogs of the Dow.”

Then, after the Dow rallied in early 1930, he borrowed $500 from his mother and started selling them short.

When the market plunged, he took profits. Whenever it rallied, he shorted again. And by the time the Dow hit rock bottom in 1932, he had over $100,000, or nearly $2 million in today’s dollars.

That was about 200 times his money.

To learn how to do something similar today with less risk, go here.

Since then, we’ve built a massive database of more than 56,000 companies and investments: stocks, ETFs, mutual funds and financial institutions.

Today, that entire database has been modernized by a team of analysts, mathematicians and data scientists, using advanced computer models.

That’s how we warned in advance about the bank failures of the 1980s.

That’s how we warned in advance about the Dot-Com bust of the early 2000s and the great Debt Crisis of 2008.

And how we warned about the inflationary crisis now sweeping the globe.

But we don’t just issue warnings; we also issue ratings, the Weiss ratings. We provide a letter grade from “A” to “E” on nearly every stock, every ETF, every mutual fund and every financial institution in America.

With those ratings, we name the stocks that are likely to fall the most, and we name the banks that are most likely to go bankrupt.

In the last debt crisis, for example, we warned about nearly every major institution that failed and we did so months in advance.

- We named Lehman Brothers as a candidate for failure 182 days before it went bankrupt.

- We named Fannie Mae over one year in advance.

- We named Citibank, Wachovia Bank and Washington Mutual Bank 51 days in advance.

- We flagged General Motors five months in advance and many more.

These kinds of on-target warnings prompted Worth magazine to say, “Weiss’s record is so good compared to that of its competitors, consumers need look no further” and …

The New York Times to say, “Weiss was the first to see the dangers and say so unambiguously.”

Barron’s wrote, “Weiss is the leader in identifying vulnerable companies.”

Louis Rukeyser of Wall Street Week wrote that “Weiss provides a tougher service.”

Chris Ruddy, founder of Newsmax and a close friend of President Trump, said, “Weiss’s prediction of the current economic crisis is uncanny.”

I think these comments demonstrate pretty clearly that our roadmap for surviving and thriving through this crisis wasn’t thrown together after the crisis began.

It’s built on a foundation of crisis investing that goes back nearly a century, to the Crash of 1929 and the Great Depression of the 1930s.

For our complete Endangered Lists, click here.

And it’s also the foundation of our endangered lists — every investment and financial institution meriting a Weiss Rating of “D+” or lower.

As of the latest count, our endangered lists include:

- 9,078 common stocks

- 9,554 ETFs and mutual funds

- 1,381 banks and credit union with insufficient capital to withstand an ordinary recession, and

- 3,580 banks and credit unions unprepared for a depression

This isn’t based on guesswork. It’s based on our massive databases — verified, official data we extract from their balance sheets, their profit and loss statements and from market price trends.

And it’s the best evidence I can give you to support one of the most important points I am conveying to you in this ebook:

This is not a “transitory” problem. It’s a financial crisis that was ready to happen long before today’s inflation —the worst in over 40 years, appeared — supposedly “out of nowhere.”

I repeat: The inflation crisis is not the cause. It is merely the trigger event, the Black Swan that swoops down from the clouds and uncovers the big debts and the big financial risks everyone was already taking.

That’s why our endangered lists are so long. And I’m sad to say, as this crisis unfolds, that’s why they’re likely to to get a lot longer.

But here’s the big payoff: As you’ll see in Chapter 6, not only can investors use our endangered list to protect themselves from losses, but they can also use them to go for life-changing profits in a market decline.

First, however, let me dispel a major myth that’s luring millions of unwitting investors into one of the greatest investment traps of all time.

Chapter 4

WARNING: If You’re Waiting for Government Bailouts To Save Your Portfolio, Read This NOW

Now, it’s time to answer that big question I raised earlier and that’s probably on your mind right now, too:

Can the government bail out the economy? Can the government fight inflation AND a recession at the same time?

Sure, the government can bail out a select group of companies. But since the last debt crisis, America’s companies have been piling up debt like there’s no tomorrow and now have over $15 trillion in notes and bonds outstanding.

And the biggest surge has been in the riskiest kind of corporate debt.

So, there’s very little the government can do to make so many financially sick companies healthy again.

There’s nothing the government can do to prevent a plunge in corporate earnings as inflation and recession strike.

There’s also nothing the government can do to stop companies from laying off millions of workers, and that’s also what we can expect. Everywhere.

There’s nothing the government can do to stop companies from cancelling their stock dividends like they did during the pandemic. Huge companies like Ford Motor, Occidental Petroleum, Boeing, Delta and Freeport-McMoRan slashed their dividends or cancelled them entirely.

And in the end, there’s nothing the government can do to stop the stock market from falling.

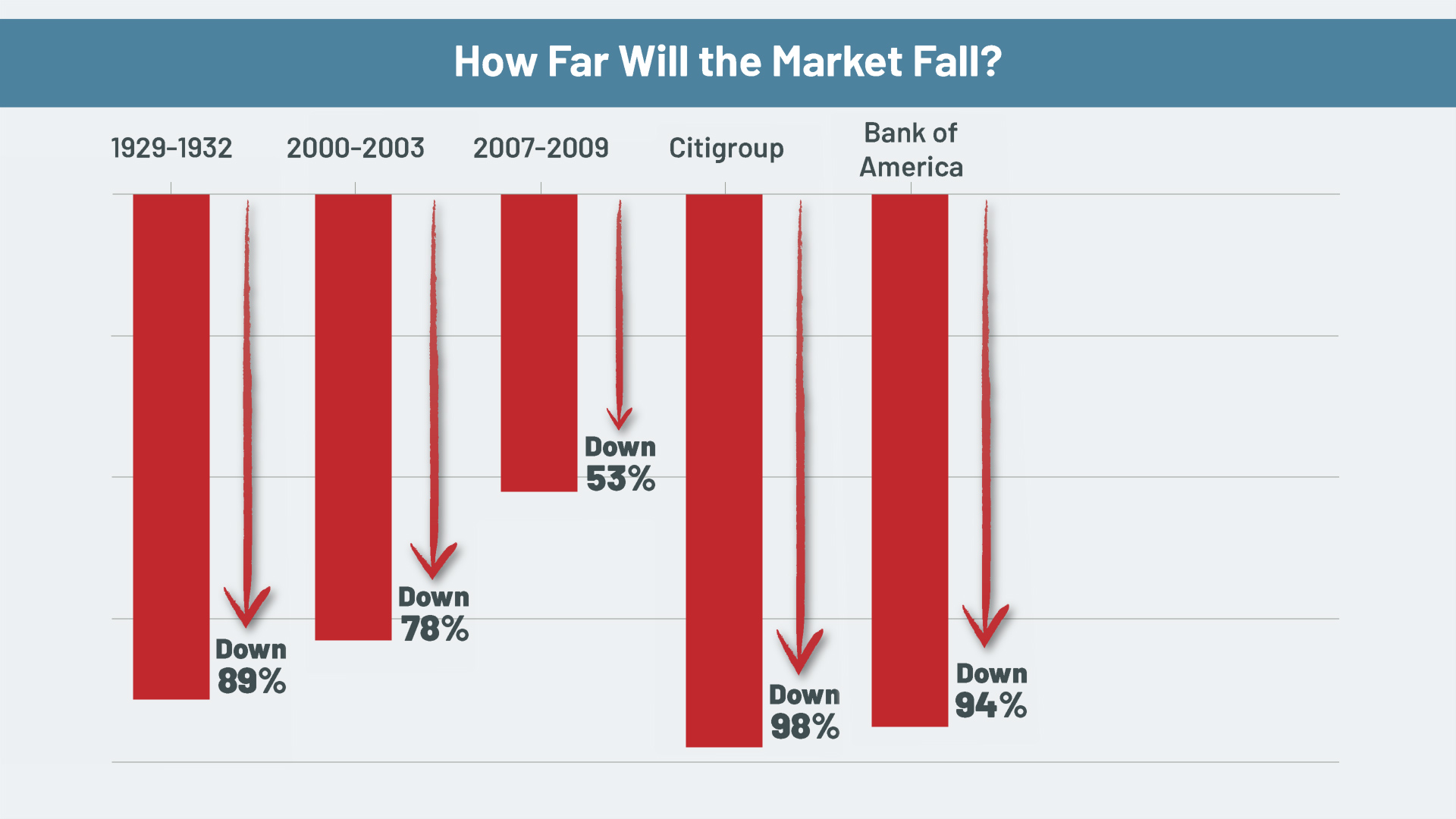

How far could the market fall? Well, here’s the history:

- In the Crash of 1929 and the big decline that followed, the average stock in the Dow Jones Industrials fell 89%.

- In the early 2000s, the average stock in the Nasdaq Composite Index fell by 78%.

- And in the 2008 Debt Crisis, the average stock in the S&P 500 fell 53%.

That’s bad enough. But notice I said “average” stock, and not all stocks are average.

- In the early 2000s, a lot of supposedly great internet stocks lost 99%, even 100% of their value.

- In the 2008 debt crisis, shares in the largest bank holding company in the United States, Citigroup, Inc fell by 98%.

- Shares in the second largest, Bank of America, fell 94%.

These giant banks and other banks were on our endangered list many months before they failed, and anyone heeding our warning would have saved a fortune back then, another reason it’s important for you to heed my warnings now.

And in the current market decline, last I checked, PayPal was down 59%, Zoom was down 60%, Roku had plunged 66%, Robinhood had crashed by 69%, Netflix had tanked 73% and Canadian Nexus was down nearly 100%.

So, if investors have stocks or ETFs, depending on which ones they own and how this crisis unfolds, history proves they could lose anywhere from half their money to almost all of their money.

Obviously, counting on the government to save your stock portfolio is not exactly a good strategy.

But here’s the biggest problem of all, the problem almost everyone on Wall Street and in Congress seems to be ignoring:

The Government Has

No Money in Reserve

The government has no savings whatsoever. Instead, it’s running a huge deficit and it’s deep in debt.

In the year 2021, even after the economy was temporarily recovering from the shock of the pandemic, the total deficit was nearly $2.8 trillion.

Even in the worst year of the Great Recession, the biggest yearly deficit was $1.4 trillion, which was then the biggest of all time.

So, last year’s deficit was TWICE as big!

Everyone should know this. But no one’s talking about it.

And no one seems to connect the dots. When the government runs such massive deficits, the only way to finance them is with funny money printed by the Federal Reserve.

And even when the Fed jacks up interest rates, that massive money printing of the recent past will fuel inflation like never before.

Of all the lessons learned from the past, this is probably the most important. Unfortunately, however, too many investors, including the so-called “pros” on Wall Street, have not yet figured it out.

That’s exactly why I’ve created this emergency ebook for you — to help you protect your assets from the storm ahead while taking steps to build wealth in the process.

In just a moment, I’ll reveal the powerful crisis-investing breakthrough my team has developed for doing just that.

But first, there’s one more major threat to your wealth, and it could be even more damaging to investor portfolios. So, I’ve dedicated the next chapter to nailing it down with no punches pulled.

Chapter 5

Sucker Rallies:

The Best Time To Sell and Make

a Fortune From the Next Decline

Starting on May 20, even as inflation continued to accelerate and the global economy continued to sink, Wall Street suddenly seemed to turn bullish. Stocks rallied, and investors breathed a sign of relief.

“This is not a bear market after all,” said the bulls. “The S&P is up, and it’s time to buy again.”

The market responded with a couple of big up days, and the mainstream media was quick to dub each one “a new bull market.”

That’s exactly what the bulls said in 1929, too.

After the initial crash in October 1929, President Hoover vigorously and repeatedly promised “the recovery is around the corner,” and investors wanted to believe him so badly, they started buying again.

So, from its low in November of 1929, the Dow rallied back to 294 on April 17, 1930. It regained 95 points or just about half of what it had lost in the crash.

But it was the next decline which turned out to be the big one. Starting in late April of 1930, the Dow plunged for nearly two full years, falling another 86%.

The bulls lost a lot of money in the crash of 1929 … and then lost a lot MORE money in the deep bear market of 1930-1932.

Meanwhile, short sellers used that second decline to make some of the greatest fortunes of the entire century, and the profits my father made are the single best example: He turned a meager $500 into more than $100,000, or about $2 million in today’s money.

Don’t be surprised if we see a similar pattern this time around.

As I showed in Chapter 3 already, even before the next phase of this crisis, we have 9,078 common stocks and 9,554 funds that are vulnerable.

Already, we have 1,381 banks and credit unions with insufficient capital to withstand an ordinary recession — not to mention 3,580 banks and credit unions unprepared for a depression.

Yes, the government can trigger big rallies in the market. But it cannot stop the stock market from falling any more than it did in the 1930s or in all the bear markets since.

And no matter what the government does, it cannot protect investors from declines in their bonds and other assets.

How to Protect Yourself From

Potentially Devastating Losses

Let’s say you own stocks that are vulnerable to a crash, especially stocks that are on our endangered list.

And suppose you’re unwilling or unable to sell them. Maybe you have a stake in the company you work for, and it’s not vested yet. Maybe the shares are in your pension plan or a family estate that you don’t control.

Plus, here’s another situation: a family business. For the most part, it would probably be very tough to sell your family business in the middle of this crisis.

So, what do you do?

This is where a hedge can be important — a firewall that investors build around their assets.

They have assets that are falling in value in this crisis. So they buy investments that are designed to go up precisely when their other assets are going down.

That’s what I mean by a hedge. And that’s what those super-profitable trades can do..

Let me give you some salient examples,

During the Great Debt Crisis, the S&P 500 fell by more than half and nearly all investors lost fortunes. But there was also a minority of investors who owned ETFs designed to profit from a market decline.

Among the 24 that existed at that time, 14 went up by 100% or more, giving investors gains of 103%, 110%, 124%, 134%, 147%, 150%, 157%, 163%, 168%, 174%, 195%, 198%, 243%, 293%.

In addition, seven of the ETFs went up by 70% or more, giving investors gains of 73%, 73%, 84%, 89%, 90%, 92% and 96%.

Now, in this crisis, I predict the profit opportunities could be even larger …

Chapter 6

How To Profit From

The Collapse of 2022

One of the most straightforward ways to make money in the Collapse of 2022 is with the simple purchase of options.

Like any other investment, the goal is to buy them low and sell them high.

The risk is absolutely limited to the small amounts invested, but the profit potential can be virtually unlimited.

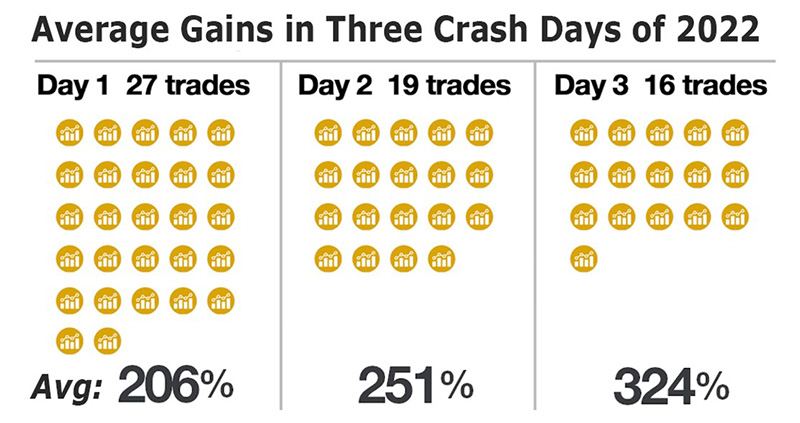

For example, in the stock market decline of 2022, we looked at three separate crash days and counted 62 distinct option trades selected by our Weiss Stock Ratings.

Each and every one could have given investors of at least 100%.

- On the first crash day, we identified 27 trades that returned gains ranging from 100% to 419%. The average gain among them was 206%.

- On the second crash day, the numbers were better: We saw 19 trades with gains ranging from 100% to 809%. Average gain: 251%.

- On the third crash day, it was even better than that: 16 trades ranging from 100% to 1,130%. Average gain: 324%.

Even if investors put up only $10,000, and even if they chose the least profitable of these trades, they could have made a profit of $10,000 on the first day, $10,000 on the second day, and another $10,000 on the third day. That's a total of $30,000 in gains in three days.

Or, if they invested those same $10,000 in just the average trades — not the best ones, mind you, just the average ones — they could have made $20,600 on day one, $25,100 on day two and $32,400 on day three. That's a total gain of $78,100.

All without reinvesting profits.

All in just three days!

We also saw trades that produced less than 100% gains. But even if you include all trades identified with our selection process in all three days, the average return was 110% on day one, 101% on day two and 149% on day three. That’s an overall average of 120% gains PER DAY.

Never forget: Options are volatile investments. So folks should only use funds that they can afford to lose. The great advantage is that the risk is strictly limited to the relatively small amounts to invest, and the profit potential can be virtually unlimited.

Our Breakthrough

Crisis-Investing Strategy

All of these trades meet the three strict requirements of our tried-and-tested all-weather strategy that can make money in almost any market environment:

- Requirement number one is strictly limited downside risk

- Requirement number two is liquidity. They have to be easy to buy and easy to sell.

- Requirement number three is high probability of success.

So exactly what is our strategy?

How can it protect you from stock market losses AND go for the opportunity to multiply your money?

First, in a declining market, we target the nation’s worst stocks, as determined by our Weiss Stock Ratings. These are the kinds of stocks that, based on 90 years of experience going back to 1929, we believe are likely to fall the most.

And never before have we seen so many: 9,078 common stocks and 1,021 ETFs on our endangered list.

Second, we narrow the list down further to stocks that are included in the S&P 500.

Third, on each stock, we select the most liquid, widely traded put options — investments designed to soar when stocks fall.

Fourth, we seek to buy the put options on a market rally, when they are cheaper.

Fifth, when the stocks fall and the puts skyrocket in value, we look to sell them for a not-so-small fortune.

Six, for assets that we believe will benefit directly from inflation, we follow a similar strategy with call options.

No complicated trades. The goal is to just buy low and sell high.

And if executed prudently, this strategy can be a godsend for investors, especially in crazy times like these.

Let’s say you hold stocks, ETFs or mutual funds in a regular stock portfolio which you are unable or unwilling to sell. Suppose you have stocks and corporate bonds in a 401(k), IRA or a variable annuity. Or perhaps you own a business that could suffer in the ongoing crisis.

If so, this strategy can go a long way toward protecting you against losses. Better yet, it has the potential to generate life-changing profits.

Here are just a few of the most recent examples of some of the larger winning trades (all on a single day) …

On Crash Day 1, April 26, 2022, we saw the following trades:

416% on Intuitive Surgical (rated C+), using a put with a strike price of $255, expiring May 13, 2022

513% on GrowGeneration (rated C-). Strike price of $6, expiring May 27

600% on SEMrush Holdings (rated D). Strike — $7.50. Expiration May 20.

1,160% on Rigel Pharmaceuticals (D-) put. Strike — $2, also expiring May 20.

Next, on Crash Day 2, April 28, the gains were even better:

483% on Editas Medicine, Inc. (rated D-) put. Strike — $11, expiring 5/6

700% on Veritone (D). Strike — $10, expiring May 20

1,000% on Accolade (D). Strike — $7.50, expiring May 20, and

1,800% on Orchid Island Capital (D). Strike — $2, also expiring May 20

Then, on Crash Day 3, May 5, investors could have made even more money with put options, including:

525% on Bed Bath & Beyond.

606% on Chewy, Inc.

1,700% on NIO Limited, and

2,200% on Blink Charging.

Among these, even with the least profitable example (Intuitive Surgical), investors could have started with $10,000 and ended it with over $50,000.

Even with the least profitable example (Intuitive Surgical), investors could have started with $10,000 and ended it with over $50,00.

With the fourth best trade (Rigel), investors could have turned $10,000 into $126,000. All in a single day.

And with the best trade (Orchid), investors could have turned that same $10,000 into $2,300,000. Also, in one day.

Bear in mind that starting with just $10,000 and making a net profit of more than $2 million like that in just a single day is NOT something folks should count on.

And I want to also remind you that we also saw trades that produced less than 100% gains. But even if you include all trades identified with our selection process in all three days, the average return was 110% on day one, 101% on day two and 149% on day three. That’s an overall average of 120% gains per day.

What makes this strategy have the potential to work especially well, however, is the strict discipline that our strategy requires.

Remember: All these trades come with downside risk that’s absolutely limited.

Chapter 7

Why at the Age of 75, I have Decided To Launch a New Service

My good friend of 20 years, Jon Markman, and I have been debating endlessly about these options — and hundreds of other opportunities we feel are begging to be snatched up in this market.

He’s the only options trader I’ve ever known who has accomplished three things: Far more winning trades than losing trades. Far bigger winners than losers. And consistency in these accomplishments year after year.

Typically, I’m strictly the publisher, and I let our senior analysts like Jon do all the work. But in this case, I could not bear to stay away from this once-in-a-generation opportunity. I wanted to be more involved.

That’s when I reminded Jon about my father and what he achieved in the great bear market of 1929-1932. So, Jon and I finally agreed: He’ll run the service and call the shots.

But I’ll also do my part. I’ll give him — and our Members — the benefit of my 50 years of experience and my father’s 60 years before me.

We have also agreed to restrict this service to a maximum of 1,000 members. We feel this is absolutely essential for two reasons.

We want to make sure that we answer every single one of your questions.

And we want to make sure investors have the best chance to get good fills on their buys and sells. Even though we use options with good trading volume and liquidity, we can’t have too many people rushing in to buy or sell.

So, we have given firm instructions to our Customer Service team to reject all orders beyond the first 1,000 members.

In prior bear markets, we sold out all available memberships to our option service for $5,000 each. And given the tremendous profits they could have made when stocks fell, I think it was a great bargain at that price.

This time around, even if the demand for our service surges in this crisis, we will not raise the price.

However, right now, we believe the market decline has just begun, and we want to give our most loyal Members a special opportunity to join before the broader public gets wind of it.

So, for a very limited time only, the price of the Weiss Ratings’ Crisis Profit Trader is only $2,500 per year. That’s a savings of $2,500 right off the bat.

And no guarantees, but we expect to come out of the gate strong.

So, let me give you a quick summary of the benefits you will get as a member of our Crisis Profit Trader.

FIRST, I will give you immediate access to our latest endangered lists — not only to look up stocks that you may own, but also to see for yourself the stocks that could generate the greatest and fastest put option profits when they crash.

SECOND, I will send you a detailed explanation of those remarkable bear-market instruments like the ones that could have turned $10,000 into $100,000 in a single crash day (even with a trade that was only the FOURTH best result so far).

For optimum profit potential, we’re putting together a starter package of three related — but different — options with varying expiration dates and strike prices.

We’ll explain what they are, how to buy them and how much to pay for them.

And in case you don’t really know what options are, we’ll include an explanation that begins with the basics and covers everything you’ll need to make this really work for you.

Most analysts give a recommendation but don’t do the necessary homework to make sure you can really act on them. We’ll tell you precisely when to get in, when to get out and at what prices.

Then we’ll keep you posted on any changes, so you’ll always have specific instructions on precisely when to close out the trade.

This is a V.I.P. exclusive service which has no ambiguities, ifs, buts, wherefores or other weasel phrases that so many analysts use to cover their you-know-whats.

THIRD — diversification.

Right now, our strategy focuses mainly on the Weiss Ratings list of Stock Market Dogs. Because, as I’ve shown you, we have seen opportunities for major fortunes being made in them right here and now. But as this crisis unfolds, it will have many repercussions on a wide range of investment sectors.

Just recently, for example, we’ve seen the sharpest decline in bond prices since 1842. As the Fed raises interest rates, we predict a far deeper decline. And there are extremely liquid put options you can buy that are not only designed to increase when bonds prices fall, but surge when bond prices crash.

Crashing bond prices is the direct and immediate consequence of surging interest rates. They go hand in hand.

Plus, surging interest rates and collapsing loan values can also hit bank stocks very hard. We’ve already seen what a 2008-style debt crisis can do to banks. If banks start failing, put options on bank stocks could see the most massive gains.

And it won’t be the first time. Back in 2008, Citicorp fell to less than $1 per share. And if you think the gains I’ve just shown you are big, wait till you see the kind of money that could be made with put options in megabanks that are going bankrupt.

We have a lot of experience in that area as well. In fact, we were the only ones that publicly named, in advance, nearly all major investment and commercial banks that subsequently failed or required a bailout.

That includes the giant Bear Stearns, which we named as a candidate for failure 102 days before it went under …

It includes the massive Lehman Brothers failure, which we predicted 182 ahead of time …

And it also includes the giant debacles at Fannie Mae and Freddie Mac, which we forecast over one year ahead of time.

Time after time, Wall Street gurus have sworn on a stack of bibles that those kinds of failures could never happen again. But now, with inflation and interest rates surging, they’re not so sure.

They’re finally beginning to recognize the truth in what we’ve been saying — that some of the most “respected” banks in the world have taken huge risks in highly leveraged debt instruments and derivatives, especially what’s called interest-rate derivatives.

And as this crisis reaches a crescendo, I predict those chickens are about to come home to roost, driving their shares to the floor and sending the value of their put options into the stratosphere.

We’re especially worried about companies that have issued big amounts of short-term IOUs (commercial paper).

On Sunday, March 15, 2020, the day before the Black Monday when the Dow plunged 2,997 points, many of these companies were already having serious difficulties rolling over their maturing short-term IOUs. If that continues, they could soon default on their obligations and sink into instant bankruptcy.

And never forget: When companies are going bankrupt, their stock falls to zero. That’s terrible for average investors. But for put option investors, it can transform a small grubstake into the equivalent of million-dollar diamonds.

FOURTH — call options. As you know, while put options surge when stocks fall, call options surge when stocks rise. And we predict that the best calls to buy will be on stocks that have historically surged the most in times of rising inflation, that have the best potential to surge like Dome and Homestake did in the early 1930s.

Plus, there’s another important lesson to be learned from my father’s experience.

The market WILL eventually recover. And on the way down, there will be several explosive rallies. All good opportunities for call options.

Imagine what will happen when inflation is finally licked, and the Fed officially announced it’s going to start lowering interest rates again.

Investors should be able to buy call options on solid companies whose stocks have been beaten to a pulp strictly because of the crisis.

Plus, to truly balance out a crisis investing portfolio, we will do more than recommend strictly options. There will also be a place for ETFs to take advantage of big moves ahead in stocks, commodities and interest rates.

FIFTH — timing.

You get our recommendations precisely when — and only when — we see what we believe is a MAJOR, first‑rate opportunity for you. We believe that when an opportunity pops, you have to grab it then and there. That’s why this service does not conform to a regular publication schedule. The market doesn’t open up opportunities according to any calendar. You could go for a couple of weeks before you get another recommendation, and then we may send you two or three recommendations in a single day.

Listen, my friend, this crisis is not waiting for you. Right now, some people still think Fed Chairman Powell will somehow find a way around surging inflation. But I say that’s a pipe dream. All the Fed’s experience in the last 13 years has been about how to print more money. And based on all logic, there’s no amount of money printing in the world that can cure inflation. It can only make it worse. And I predict it can only lead to one thing: More Fed Fiascos, more interest rate shocks and more crash days in the market.

The thing is, to take advantage of the next crash day, you have to have your options in place, sitting there BEFORE the next decline hits.

Don’t expect to wake up one morning and think: “Oh. Martin and Jon were right. The market IS crashing again. Let me jump on board now.” By then, it could be too late.

At this very early stage of the crisis, no one can say for sure how much inflation will soar, how quickly the Fed will raise rates or how far the stock market will fall.

Plus, it’s far too soon to say when a true recovery will begin, how strong it will be, and how quickly stocks will bounce back. But I can say one thing with certainty: This crisis is — and will continue to be — so rich with opportunities for option investors, the potential for profits is far greater than anything I’ve ever seen in my lifetime.

As we’ve seen, in just the three first crash days of this year, investors could have made AVERAGE gains of 206%, 251% and 324%. Each in one day.

So, here’s my promise to you: If, after your first year, you cannot make at least ten times your money by following the trading recommendations in our Crisis Profits Trader, let us know, and we will give you a second year free, worth $5,000.

That’s like a $5,000 credit to your account!

But I want to warn you, there are three very logical and necessary conditions to this offer.

First, this offer is limited to strictly our V.I.P. Members, based on their history with Weiss Ratings and our related services.

Second, it is strictly limited timewise. If you do not respond with this grand finale of our three-part emergency series, you could be very disappointed.

Third, we have allocated a total of 1,000 memberships. Total. Then, once the 1,000 slots are gone, that’s it.

The first time we offered a service like this in a crisis environment, we also limited it to 1,000 Members paying $5,000 each. It sold out in seven days. We even had to return checks that came in the mail. And back then, we had only 30,000 readers who received the offer.

This time, we have over 100,000 active readers. And we fully expect that more than 2% may want to subscribe to our Crisis Profit Trader. So, all 1,000 slots will be sold out very soon.

Once these are gone, that’s it. Unless you want to be placed on a waiting list, it will be impossible to join. With the market already in crisis and more crashes on the way, I don’t want to disappoint you.

If you want to become a Member, it’s critical that you send your annual fee in now, before we run out of the available slots. To make sure, I suggest you pick up the phone and call us toll-free at 1-877-934-7778.

And if our phone lines are backed up due to a surge in demand, just click here to sign up instantly online.

I know that, even with everything going on today, the vast majority of Americans will fail to heed my warnings and fail to get ready for the next phase of this crisis.

But I sincerely hope, for you and your family’s sake, that you’re not one of them. The precautions required to weather this storm are not difficult.

And even if the storm turns out to be less severe than we fear, the worst that’ll happen is that you’ll sleep better at night and you’ll receive our guidance through the peaks and valleys.